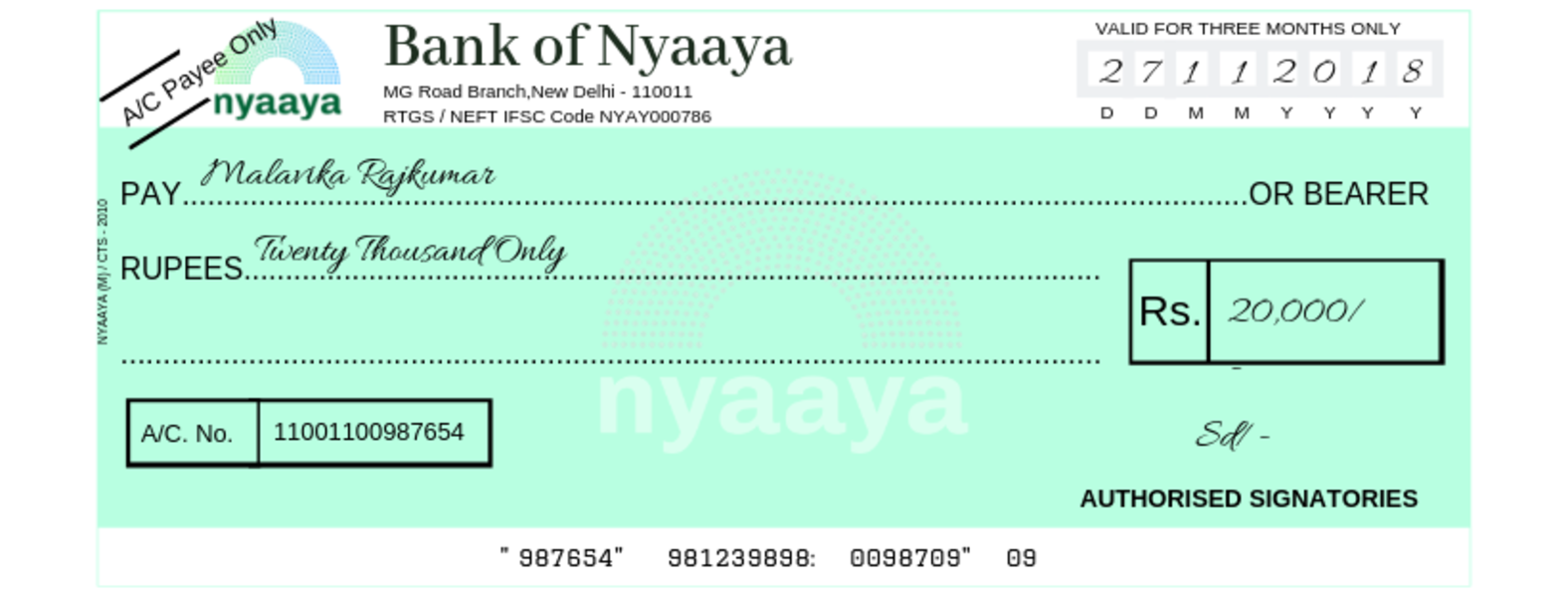

Crossing a cheque means that it cannot be transferred to anyone else. In such cheques, you have to draw two parallel lines on the top left corner of the cheque and you can write the words “Account Payee Only” or “Not Negotiable” with it.

For illustration purposes only

These cheques cannot be encashed at the cash counter of a bank but can only be credited to the payee’s account.

These cheques are crossed to minimise the risk of misappropriation or loss of identity. Since crossed cheques are not payable at the counter and the amount is credited into the bank account of the payee, this is a safer way of transferring money as compared to an uncrossed or an open cheque on which no amount of money has been written.

A crossing may also be made where the name of the bank is indicated on the cheque, to restrict the payment. For example, if a cheque is made in the name of B and a crossing “Bank of Baroda” is made on the cheque, the cheque would be payable only to the account of B with Bank of Baroda and no other bank

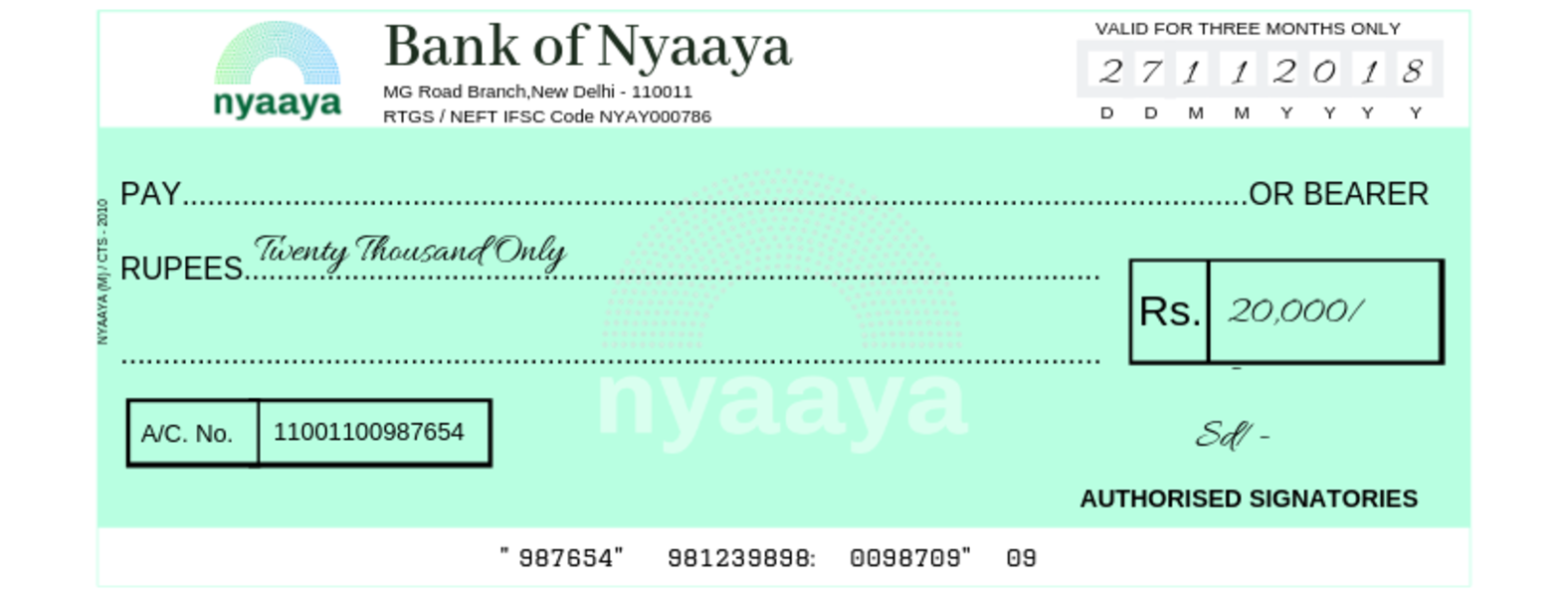

An uncrossed cheque or an open cheque is a cheque that has not been crossed with two parallel lines on the top left corner. Such cheques can be encashed at any bank. You can collect the money for the cheque from the bank counter. It can also be transferred to the bank account of the person who presented the cheque.

If you have a bearer cheque, then you can present it to the bank and get the cash amount written on it. Any person can give the cheque and collect the money written on it.

For Example: If Sanjana presents the bearer cheque at the bank counter for encashment, the amount will be paid in cash to her.

For illustration purposes only

Usually the words “or bearer” are printed on the leaf of the cheque. It can be issued to a third party in the third parties name or in the name of the firm. A bank cannot refuse payment of this kind of cheque across the counter.

Since anyone can present it to the bank and collect the cash amount written on it, these are risky in nature. So in a situation where you lose it, there may be a chance of someone else presenting it to the bank and collecting money.

If a cheque is crossed then it automatically is not a bearer cheque.

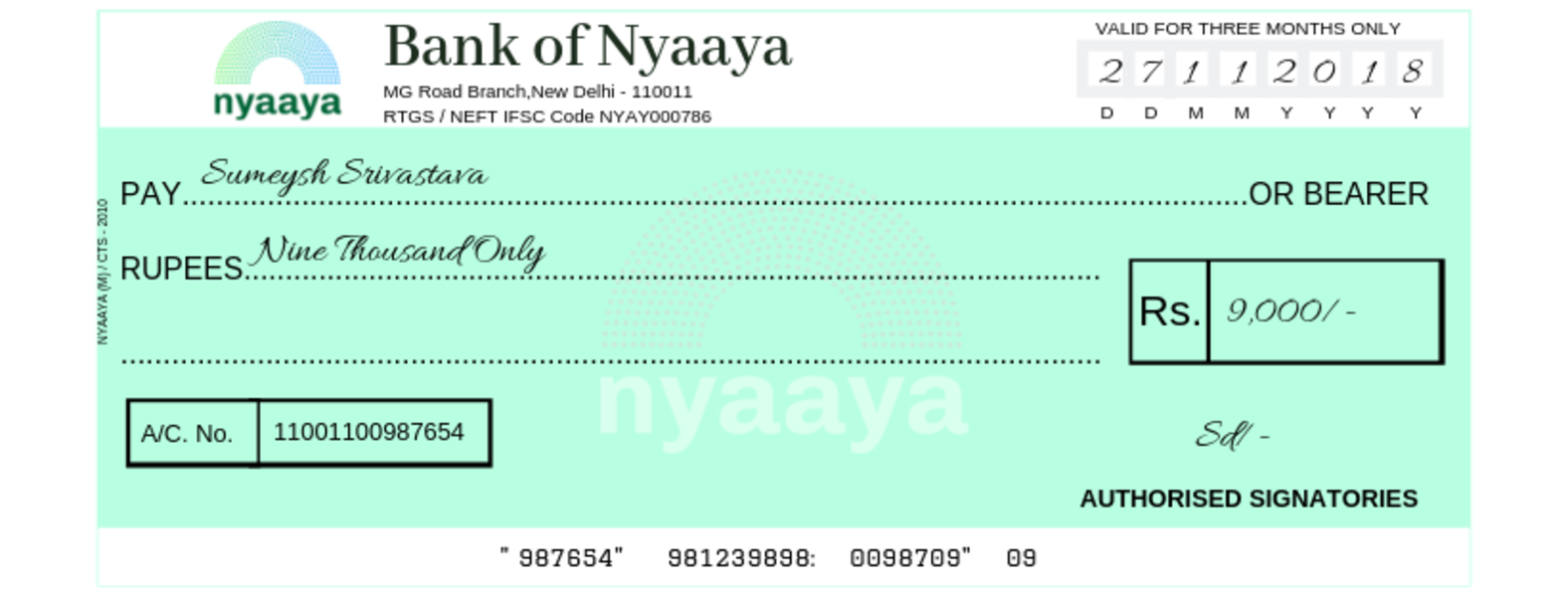

An order cheque is a cheque where only the person or party in whose name the cheque has been drawn, can withdraw the cash. The person collecting the cheque has to give an identity proof to encash the cheque. In such cheques, you have to strike out the words “or Bearer” and specify the person to whom the cheque is written for. Only then will it become an order cheque.

For illustration purposes only

For Example: If Sumeysh’s name is written on the cheque, only he can present the cheque for payment and get it encashed. No one else will be allowed to withdraw the amount.

The payee can transfer an order cheque to someone else by signing their name on the back of it. This is known as endorsing of a cheque.

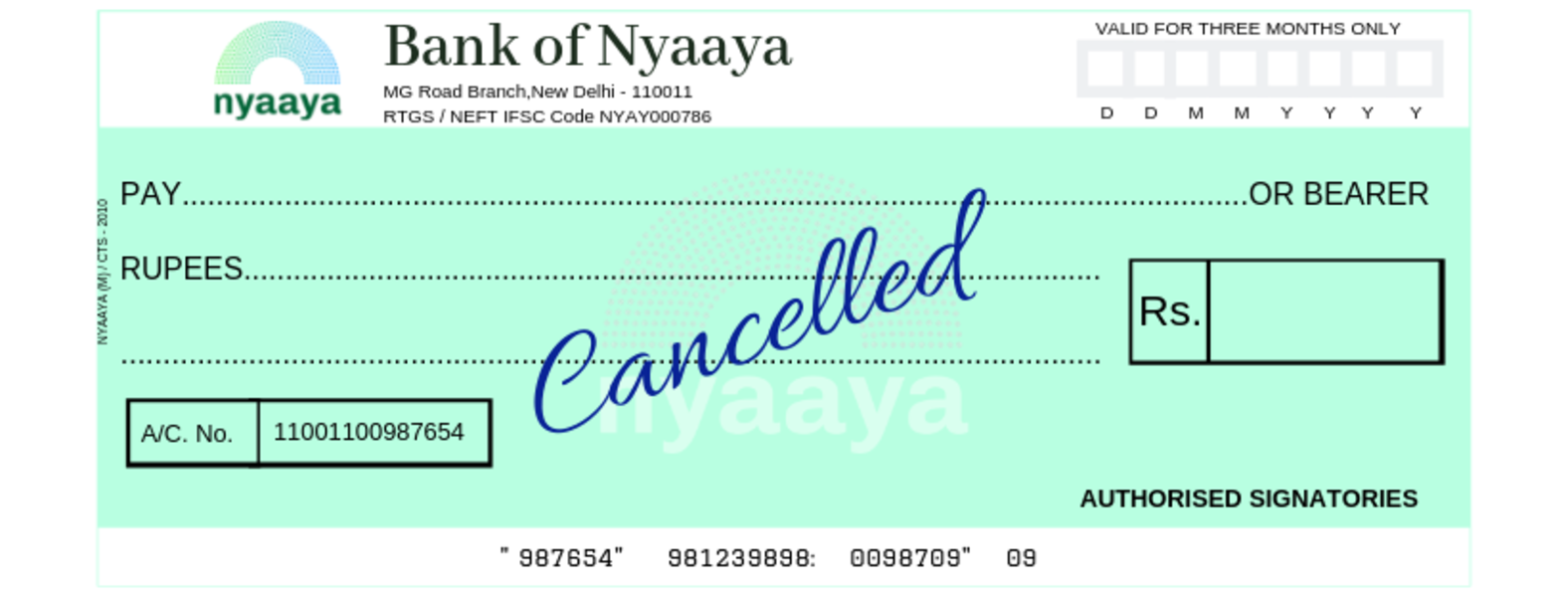

If the words “cancelled” has been written on the cheque then, it is known as a cancelled cheque. Usually, the word cancelled is written across the cheque leaf in a big font, so that it is clear to anyone seeing the cheque, that it is a cancelled cheque. The purpose of giving anyone a cancelled cheque is to let someone, for example, your employer, know your bank account details such as:

There are certain precautions to be taken by customers when dealing with cheques.

Ensure that the cheque has CTS 2010 written on it.

Preferably use image-friendly coloured inks like blue and black while writing cheques. Avoid using inks like green and red.

You should also avoid any alterations/corrections once you have written the cheque. Preferably, use a new cheque leaf if you need to make any alterations/corrections as the cheque may be cleared through image based clearing system.

Make sure that your signature on the cheque is the same as the signature in the bank records. Otherwise, your cheque may be declined and the bank may penalize you.

Banks should use “CTS 2010” cheques which are not only image friendly but also have more security features.

Using Stamps on Cheques With Care

Banks should exercise care while affixing stamps on the cheque forms, so that it does not interfere with the material portions such as date, payee’s name, amount and signature. The use of rubber stamps, etc, should not overshadow the clear appearance of these basic features in the image.

Scanning of CTS Cheques by Banks

It is necessary to ensure that all essential elements of a cheque are captured in an image during the scanning process and banks have to exercise appropriate care in this regard.

There are several reasons that could cause problems in cheque processing and lead to cheque bouncing. But not all of them warrant legal action. For example, a cheque could bounce if the sign of the drawer does not match with the account.

A detailed list of these reasons has been provided by the Reserve Bank of India in Annexure D of the Uniform Regulation and Rules for Bankers Clearing Houses.

When you fill a cheque either without the authorisation of the account holder or exceed the amount you were authorised to fill then you have committed a crime. This is known as forging a cheque.

The punishment for this offence is jail time up to two years and/or a fine.

Examples

Mustafa took a blank cheque from Adrija and without her knowledge added in an amount of Rs. 10,000 along with falsifying her signature. He presented this cheque to the bank for payment. In this case, Mustafa has committed forgery.

Adrija gave Mustafa a signed cheque and authorised him to put in an amount only up to Rs. 10,000. Mustafa fills in Rs. 20,000 and presents it to the bank for payment. Mustafa has committed forgery.

One of the ways in which a cheque is said to have been ‘bounced’ or ‘dishonoured‘ is when it is deposited or presented for payment but could not be encashed by the holder of the cheque.

There are several reasons why a cheque would bounce. However, not all of them amount to a crime. It is a crime if the cheque bounced either because of:

Insufficient funds in the drawer’s account, or

The payment for the cheque was stopped by the bank on the request of the issuer of the cheque.

Examples: ‘A’ issues a cheque to ‘B’ for Rs. 1,000. When B deposits the cheque in the bank, the bank informs him that ‘A’ does not have Rs. 1,000 in her account to pay ‘B’ with. The cheque has been dishonoured. ‘A’ issues a cheque to ‘B’ for Rs. 1,000. Before B can deposit the cheque, ‘A’ issues instructions to her bank to stop payment of the cheque without the knowledge and consent of ‘B’. When ‘B’ tries to encash the cheque, he cannot do so. The cheque has been dishonoured.