A valid cheque is one that can be presented to the bank in order to receive money from the drawer’s account. The validity of the cheque will depend upon the date it was issued. Once a date has been written on a cheque at the time of issuance, it will only stay valid for up to 3 months from that date. For example, if a cheque has been issued on 1st January, 2019, then it will only be valid till 1st April, 2019. There are two broad categories of valid cheques:

Optional Grouping: Types of Cheques

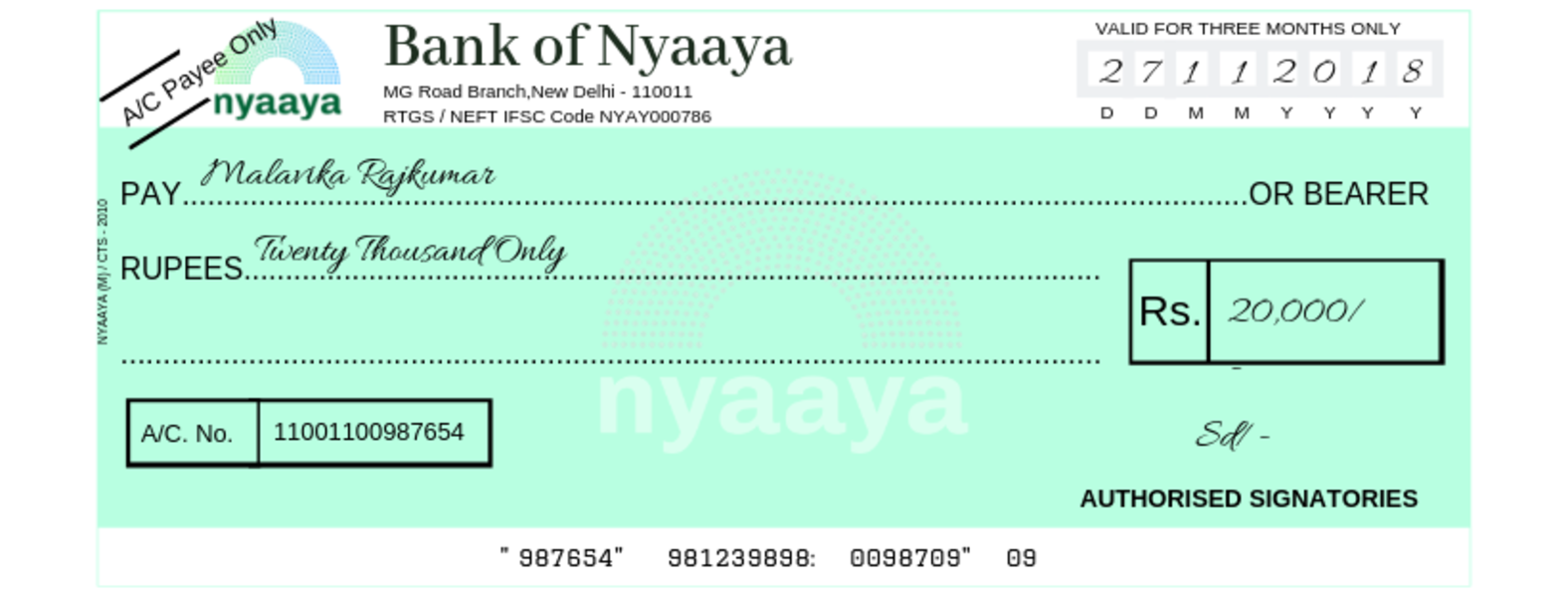

Crossed Cheque

Crossing a cheque means that it cannot be transferred to anyone else. In such cheques, you have to draw two parallel lines on the top left corner of the cheque and you can write the words “Account Payee Only” or “Not Negotiable” with it.

For illustration purposes only

These cheques cannot be encashed at the cash counter of a bank but can only be credited to the payee’s account.

These cheques are crossed to minimise the risk of misappropriation or loss of identity. Since crossed cheques are not payable at the counter and the amount is credited into the bank account of the payee, this is a safer way of transferring money as compared to an uncrossed or an open cheque on which no amount of money has been written.

A crossing may also be made where the name of the bank is indicated on the cheque, to restrict the payment. For example, if a cheque is made in the name of B and a crossing “Bank of Baroda” is made on the cheque, the cheque would be payable only to the account of B with Bank of Baroda and no other bank

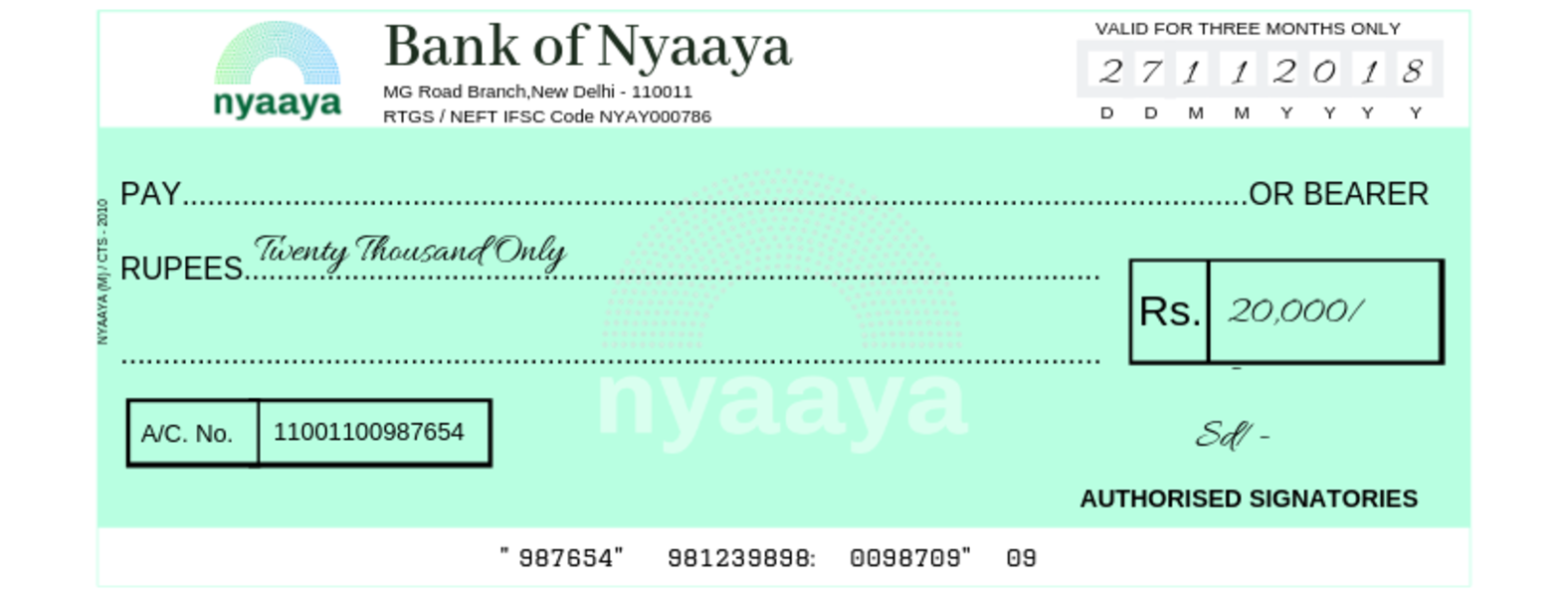

Uncrossed or open cheque

An uncrossed cheque or an open cheque is a cheque that has not been crossed with two parallel lines on the top left corner. Such cheques can be encashed at any bank. You can collect the money for the cheque from the bank counter. It can also be transferred to the bank account of the person who presented the cheque.

Types of uncrossed/open cheques are:

Bearer cheque

If you have a bearer cheque, then you can present it to the bank and get the cash amount written on it. Any person can give the cheque and collect the money written on it.

For Example: If Sanjana presents the bearer cheque at the bank counter for encashment, the amount will be paid in cash to her.

For illustration purposes only

Usually the words “or bearer” are printed on the leaf of the cheque. It can be issued to a third party in the third parties name or in the name of the firm. A bank cannot refuse payment of this kind of cheque across the counter.

Since anyone can present it to the bank and collect the cash amount written on it, these are risky in nature. So in a situation where you lose it, there may be a chance of someone else presenting it to the bank and collecting money.

If a cheque is crossed then it automatically is not a bearer cheque.

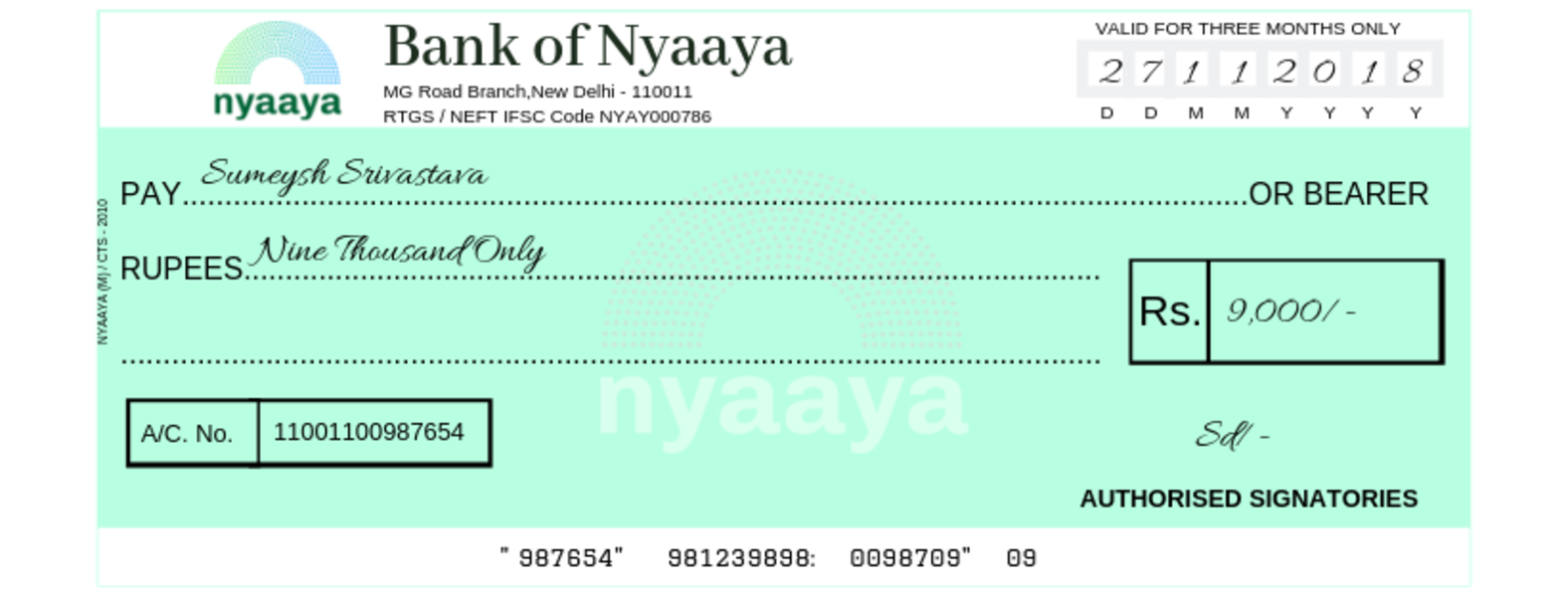

Order Cheque

An order cheque is a cheque where only the person or party in whose name the cheque has been drawn, can withdraw the cash. The person collecting the cheque has to give an identity proof to encash the cheque. In such cheques, you have to strike out the words “or Bearer” and specify the person to whom the cheque is written for. Only then will it become an order cheque.

For illustration purposes only

For Example: If Sumeysh’s name is written on the cheque, only he can present the cheque for payment and get it encashed. No one else will be allowed to withdraw the amount.

The payee can transfer an order cheque to someone else by signing their name on the back of it. This is known as endorsing of a cheque.

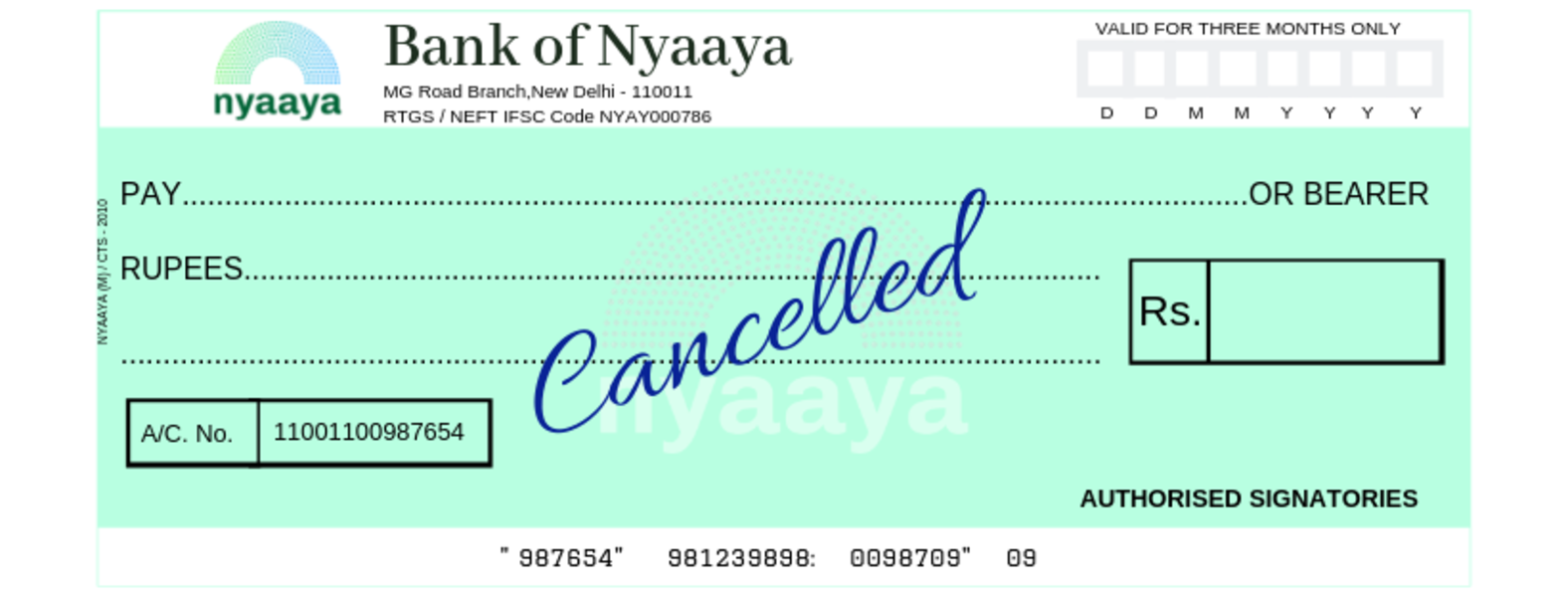

Cancelled cheque

If the words “cancelled” has been written on the cheque then, it is known as a cancelled cheque. Usually, the word cancelled is written across the cheque leaf in a big font, so that it is clear to anyone seeing the cheque, that it is a cancelled cheque. The purpose of giving anyone a cancelled cheque is to let someone, for example, your employer, know your bank account details such as:

- Your full name,

- IFSC Code,

- Bank Account Number etc.

For illustration purposes only