Each bank will have their own policy on cheque collection. You can ask your bank or check their website for their policy.

Theme: Cheques

Someone issued a cheque to me but the account was closed before I could encash it. Is this cheque bouncing?

Yes, this is cheque bouncing. If the account of the person who issued you the cheque is closed, then it is an act of cheque bouncing.

What does Account Payee on the side corner of the cheque mean?

If “Account Payee” is written between the crossed lines on the corner of the cheque, it means that when the cheque is presented to the bank by you, the cheque amount will be transferred to your bank account only. You cannot get the cheque amount in cash over the counter.

What does “or bearer” on a cheque mean?

When a cheque has no name written in the payee section and the “or bearer” has not been crossed out, it is called a bearer cheque. To know more about bearer cheques, please refer to this.

Are there any other consequences to dishonor of cheque that I can face in terms of banking privileges with my respective bank?

The RBI (Reserve Bank of India) allows each bank to decide the consequences of repeated cheque bounces. So please check with your bank with regards to specific consequences for repeated cheque bounces.

Is it possible that the bank can misplace my cheque after I have presented it to them for encashment?

It is possible for the bank to misplace your cheque either during the clearing process or at the paying bank’s branch. In such situations the bank should do the following:

- The bank should immediately inform the customer who presented the cheque.

- The customer is entitled to be reimbursed by banks for related expenses for obtaining duplicate instruments and also interest for reasonable delays in obtaining the same.

As soon as the bank informs the customer that the cheque has been lost, then the customer can take precautions and inform the drawer of the cheque to stop the payment of the cheque.

It may however be noted that the probability of losing the physical instrument in the hands of paying bank is remote, in the locations covered by CTS as clearing is undertaken on the basis of images.

Will I receive an acknowledgement for cheque deposited in a bank for collection?

There are two types of facilities that banks provide for cheques:

- They provide a drop-box facility where you can drop-off your cheque. You will not get an acknowledgement for a cheque dropped at the drop-box.

- They also have collection counters where you can get an acknowledgement when you give the cheque for collection at the bank branch’s counter.

I issued a cheque to my landlord at the beginning of the month for rent and when he en-cashed the cheque there was no money in my bank account. Can I be held liable?

Yes, you can be held liable for cheque bouncing. Typically a cheque is valid for 3 months from the date on which it is issued. When you make a promise to your landlord to pay your rent through a cheque, it is understood your promise is good for 3 months. Even if your intention was to pay your rent when you wrote the cheque, but a few days later, your account balance went below the amount required to pay the rent cheque on the day your landlord presented the cheque for payment, you have still committed an illegal act. The relevant factor is not your intention to pay when you wrote the cheque, but whether your promise can be honoured on the day your landlord presents the cheque at his bank.

I lost my cheque return memo. What do I do?

Write to your bank requesting another cheque return memo. Your bank will give you another copy of the cheque return memo which will be in duplicate.

If I have filed a cheque bouncing case against someone, can I ask the Court for some interim compensation?

Yes, if you have filed a cheque bouncing case against someone, you can apply for interim compensation to be given to you. This compensation would be 20 percent of the amount of cheque that was bounced. Once the court passes the order for the compensation, you should be paid within 60 days by the accused person. In exceptional cases they can even pay you in 90 days.

If the final court order in the case is in your favour, the award amount that you will receive will be after deducting the compensation amount paid in the beginning of the case. But in case the final order is not in your favour, you must return the initial compensation amount with interest.

What is the format in which I should send a notice to the issuer/drawer of the cheque?

Any demand made after the dishonour of cheque will constitute a notice. It is not necessary that the notice should be sent by Registered Post alone, it could be sent even by fax. It is not necessary that the notice should be in any particular form or style. What is essential is that there should be a demand to pay the dishonoured cheque amount.

How do cheques work?

Let’s understand how cheques work. A cheque is a promise made in writing by one person to another to unconditionally pay a specified amount of money. However, you can also write a cheque to yourself.

For example, if Amit owes Asha Rs. 10,000, he can give Asha a cheque of Rs. 10,000. When Asha presents this cheque to the bank, she will receive Rs. 10,000 as cash or in her bank account. Rs. 10,000 will be deducted from Amit’s account.

In technical terms, as used by bankers and lawyers, a cheque is also referred to as and is a type of a ‘Negotiable Instrument’.

The different parties involved in dealing with a cheque are:

- The issuer of the cheque (Drawer)

- The payee/holder of the cheque and

- The bank (Drawee)

Intention of Drawer of Cheque

If a cheque you issued has bounced, intention of the drawer of the cheque does not matter. It is irrelevant whether or not you intended to for your cheque to bounce. Even if the bouncing of the cheque has happened without ill intent or malice it is considered illegal and a crime under the law.

Importance of Signature on a Cheque

The signature on a cheque means that the person who has signed it is giving permission to the bank to take money out of his or her account. When you give a cheque to the bank, keep in mind the following:

- Make sure the signature of the person who issues the cheque matches with the signatures in his bank records.

- If your signature on the cheque mismatches with your signature in the bank records, then the bank can fine you for this.

A signature mismatch can attract a penalty if the bank decides to return your cheque.

Encash a cheque

Follow these steps to encash a cheque.

Analyse the type of cheque that has been issued to you.

Bearer Cheque

If it is a bearer cheque, then there will be no name written on the cheque. You can:

- Go to any branch (in the city) of the bank that the cheque belongs to

- Present it for clearance

- The bank teller, will verify the details on the cheque and clear it

- The cheque will be cleared then and there and you will get the cash

Order Cheque

If it is an order cheque it will have your name written on it. You can:

- Go to any branch in the city of the bank that the cheque belongs to and

- Present it for clearance

- The bank teller, will verify the details on the cheque and clear it -The cheque will be cleared then and there and you will get the cash

Account Payee Cheque

If it’s an account payee cheque, then write your name, your account number and contact number at the back of the cheque, fill the deposit slip and exercise any of the following options.

Bank/ATM Dropbox Deposit

You can either go to an ATM of your bank or directly go to any branch of your bank where you have an account.

If the ATM of your bank has cheque deposit slips and a drop box, the most convenient option is to do the following:

- Fill in the cheque deposit slip. A deposit slip has two parts; the smaller part that you fill and keep with yourself and the bigger part that you fill and deposit in the drop box, along with your cheque.

- Tear your portion of the slip and keep it with yourself

- Pin the cheque and other part of the deposit slip

- Drop in into the ATM dropbox.

However, with this dropbox option, you will not receive an acknowledgement from the Bank of the receipt of your cheque and deposit slip. This means that if the cheque is lost by any chance, you will not be able to find out about the status of the cheque from the bank. However, you can still stop your cheque through internet banking or by writing a letter to the Bank.

If the ATM of your bank branch does not have the dropbox facility, then you have to go to the bank and drop the cheque. The detailed procedure is given below.

ATM Deposit

Some ATM’s have the option to deposit the cheque in the ATM machine itself. Please follow the procedure set out in the machine and deposit it accordingly.

Bank Deposit

- Fill a cheque deposit slip

- Get the appropriate cheque deposit slip form amongst the various slips that are usually kept at the dropbox area of the branch. Make sure you have the proper slip.

- Carefully fill in your bank account number, branch name, cheque amount etc. – Sign at the appropriate place. Also fill in details of the cheque, such as cheque number, bank from which the cheque is drawn, amount, date on which such cheque was drawn etc. Make sure that you fill in these details in the relevant places.

- Tear your portion of the slip, pin both cheque and the other part of the slip and drop them in the dropbox.

Cheque Clearing

Cheque Clearing means processing a cheque from one bank to another by transferring the amount mentioned on the cheque to the payee’s account. The two most commonly used forms of cheque clearing systems are:

Cheque Truncation System

Cheque truncation is a form of cheque clearing system. It digitises a physical paper cheque into a substitute electronic form. This is done for transmitting the amount of money mentioned on the cheque to the paying bank. This is also referred to as ‘Local Cheque Clearing’.

In this process, an electronic image of a cheque is sent by the clearing house to the paying branch. This image contains all relevant information like date of presentation of the cheque, presenting bank, data on the MICR [Magnetic Ink Character recognition], etc. By this process, the paying branch gets these details automatically.

This is a much simpler and a faster process of clearing a cheque than physically transferring a cheque from one bank to another. Since cheque truncation speeds up the process of collecting cheques it results in better service to customers and reduces the scope of loss of cheques in physical transit. This process is faster and more secure.

Endorsing cheques

Endorsing cheques means that if you have an order cheque then you can endorse it to someone else. Endorsing means the payee can use the same order cheque to pay to someone else (the creditor) by writing that person’s name on the back of the cheque and signing it. When a person gets an endorsed cheque, he can collect the cash himself.

Example: Rahul gave a cheque to Raju. If Raju wants to endorse that cheque to Divya, he has to write Divya’s name behind the cheque and sign it.

Endorsing in favour of multiple people

A cheque can be endorsed any number of times. This means that a person can give it to someone, who can give it to someone else and the same can be continued multiple times. However, the bank may seek further information before crediting the amount in the account of the last person to whom the cheque is endorsed i.e. the final beneficiary of the cheque.

For Example

Jeet issued a cheque in favor of Sohini and Sohini decides to endorse the cheque to Adrija, by writing Adrija’s name behind the cheque given to her. Adrija can endorse the same cheque to any other person in the same way. Now, if the cheque has finally come to Param then the bank could ask for details (such as ID card) from Param when he approaches the bank to receive the cash.

Cheque that cannot be endorsed further

If a cheque is crossed and “Account Payee Only” or “Not Negotiable” is written on it, then it means that the cheque cannot be endorsed to anybody else. The cheque has to be necessarily collected by the banker of the payee on his behalf.

For Example

Simran has issued a cheque in favour of Namrata. But, she has written “Account Payee Only” or “Not Negotiable” and crossed the cheque. Then, Namrata cannot endorse it further.

Speed Clearing for Outstation Cheques

Cheques can be issued to a person holding a bank account in a bank branch in the same city or outside. When the cheque is issued to a person outside the same city then it becomes an outstation cheque.

Speed Clearing is a process that makes it possible to clear such cheques, locally. With the help of MICR and Core Banking System (CBS), the entire process of clearing such cheques has become easier and faster. It is also referred to as ‘Grid-Based Cheque Truncation System’.

Before the Speed Clearing Process existed, if you deposited an outstation cheque at your bank, it would first go to the local clearing house in your city and then the cheque would be physically sent to the outstation branch to process the payment. Now, with speed clearing, the cheque is sent to the local branch of the drawee bank for clearance.

Hence, clearance becomes faster with the Speed Clearing System.

Valid cheques

A valid cheque is one that can be presented to the bank in order to receive money from the drawer’s account. The validity of the cheque will depend upon the date it was issued. Once a date has been written on a cheque at the time of issuance, it will only stay valid for up to 3 months from that date. For example, if a cheque has been issued on 1st January, 2019, then it will only be valid till 1st April, 2019. There are two broad categories of valid cheques:

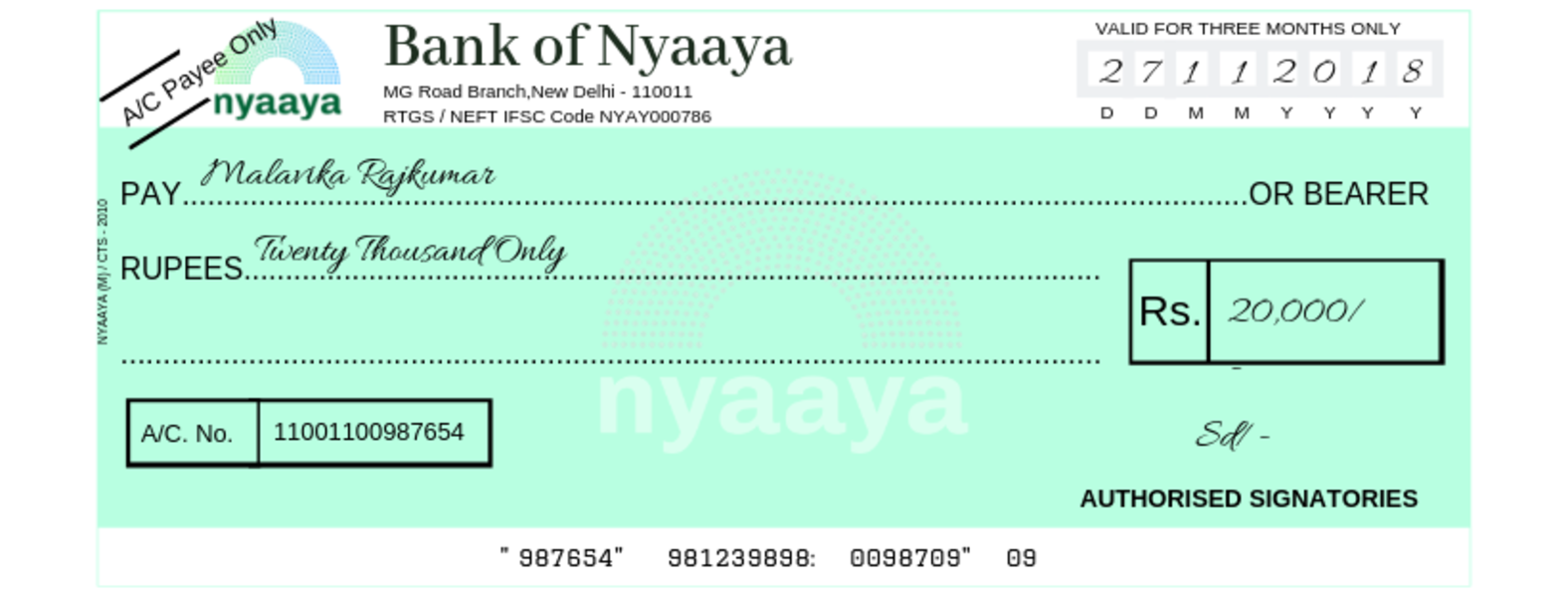

Crossed Cheque

Crossing a cheque means that it cannot be transferred to anyone else. In such cheques, you have to draw two parallel lines on the top left corner of the cheque and you can write the words “Account Payee Only” or “Not Negotiable” with it.

For illustration purposes only

These cheques cannot be encashed at the cash counter of a bank but can only be credited to the payee’s account.

These cheques are crossed to minimise the risk of misappropriation or loss of identity. Since crossed cheques are not payable at the counter and the amount is credited into the bank account of the payee, this is a safer way of transferring money as compared to an uncrossed or an open cheque on which no amount of money has been written.

A crossing may also be made where the name of the bank is indicated on the cheque, to restrict the payment. For example, if a cheque is made in the name of B and a crossing “Bank of Baroda” is made on the cheque, the cheque would be payable only to the account of B with Bank of Baroda and no other bank

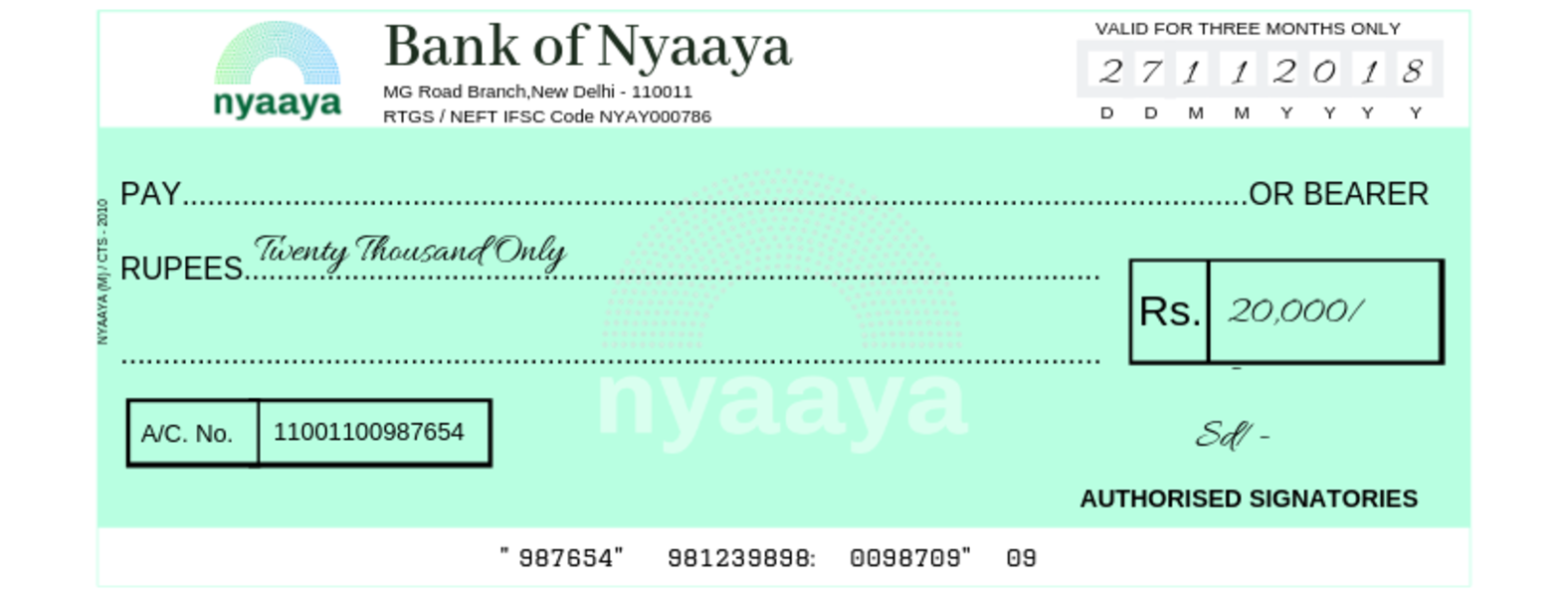

Uncrossed or open cheque

An uncrossed cheque or an open cheque is a cheque that has not been crossed with two parallel lines on the top left corner. Such cheques can be encashed at any bank. You can collect the money for the cheque from the bank counter. It can also be transferred to the bank account of the person who presented the cheque.

Types of uncrossed/open cheques are:

Bearer cheque

If you have a bearer cheque, then you can present it to the bank and get the cash amount written on it. Any person can give the cheque and collect the money written on it.

For Example: If Sanjana presents the bearer cheque at the bank counter for encashment, the amount will be paid in cash to her.

For illustration purposes only

Usually the words “or bearer” are printed on the leaf of the cheque. It can be issued to a third party in the third parties name or in the name of the firm. A bank cannot refuse payment of this kind of cheque across the counter.

Since anyone can present it to the bank and collect the cash amount written on it, these are risky in nature. So in a situation where you lose it, there may be a chance of someone else presenting it to the bank and collecting money.

If a cheque is crossed then it automatically is not a bearer cheque.

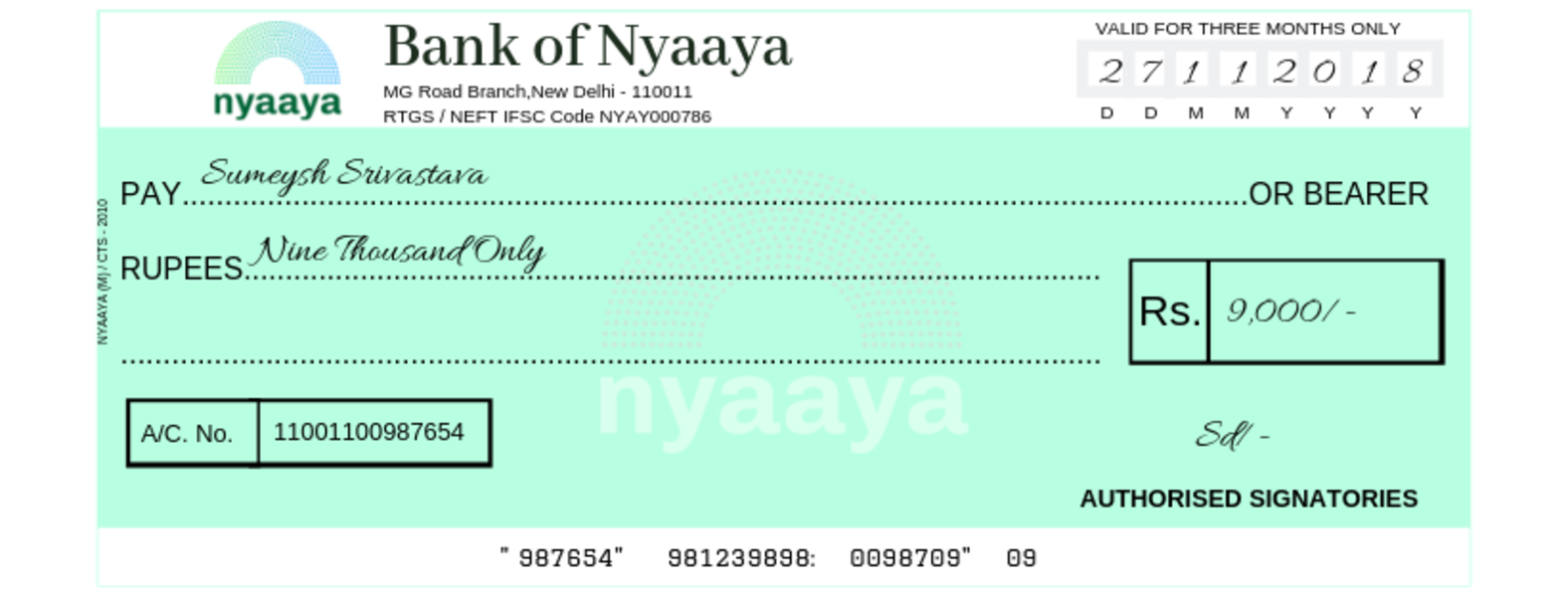

Order Cheque

An order cheque is a cheque where only the person or party in whose name the cheque has been drawn, can withdraw the cash. The person collecting the cheque has to give an identity proof to encash the cheque. In such cheques, you have to strike out the words “or Bearer” and specify the person to whom the cheque is written for. Only then will it become an order cheque.

For illustration purposes only

For Example: If Sumeysh’s name is written on the cheque, only he can present the cheque for payment and get it encashed. No one else will be allowed to withdraw the amount.

The payee can transfer an order cheque to someone else by signing their name on the back of it. This is known as endorsing of a cheque.

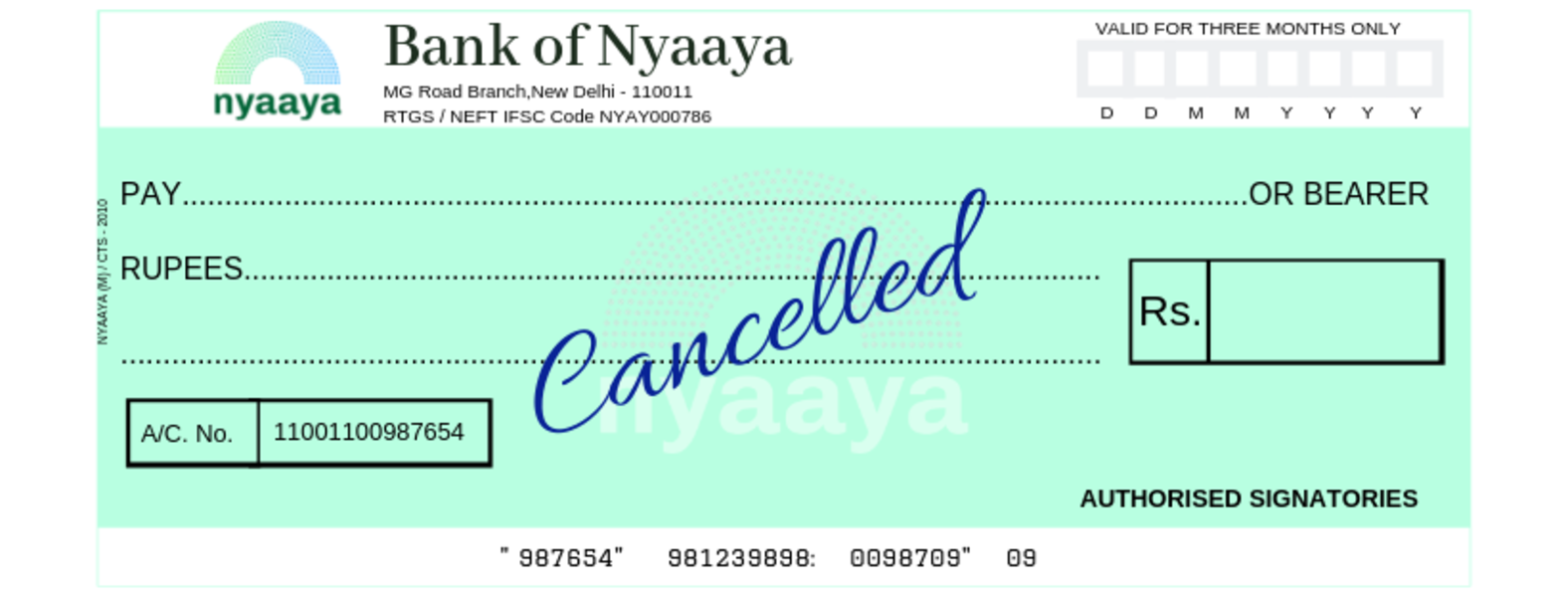

Cancelled cheque

If the words “cancelled” has been written on the cheque then, it is known as a cancelled cheque. Usually, the word cancelled is written across the cheque leaf in a big font, so that it is clear to anyone seeing the cheque, that it is a cancelled cheque. The purpose of giving anyone a cancelled cheque is to let someone, for example, your employer, know your bank account details such as:

- Your full name,

- IFSC Code,

- Bank Account Number etc.

For illustration purposes only